How Inheritance & Gift Tax (CAT) Works in Ireland

When transferring wealth in Ireland, whether during a lifetime or upon death, it's important to understand how Capital Acquisitions Tax (CAT) applies. This tax is charged on gifts and inheritances, and it affects both the giver (disponer) and the recipient (beneficiary). Proper planning around CAT can help reduce tax liabilities and ensure a smooth transfer of assets to the next generation.

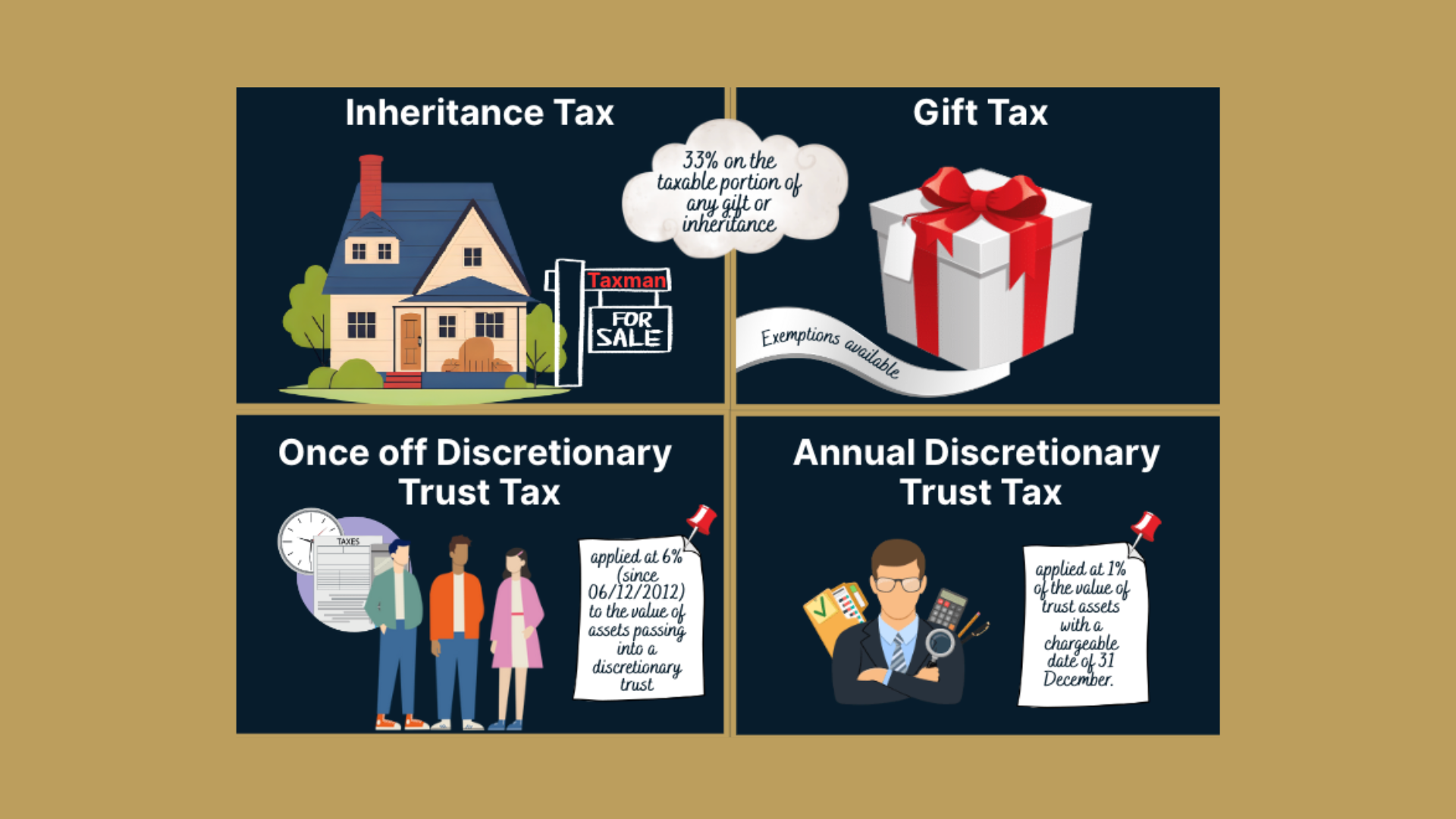

What is Capital Acquisitions Tax (CAT)?

CAT is a tax levied on the recipient of a gift or inheritance. It is charged at a standard rate of 33% on the taxable value of the asset received above certain thresholds, which vary based on the relationship between the disponer and the beneficiary.

Key Concepts of CAT

To understand how CAT works, it’s useful to be familiar with the following terms:

- Disponer: The person giving the gift or bequest.

- Beneficiary: The person receiving the gift or inheritance.

- Group Thresholds: Tax-free amounts that vary based on the relationship to the disponer.

- Taxable Value: The value of the gift or inheritance, minus allowable exemptions and reliefs.

CAT Group Thresholds (as of 2025)

There are three threshold groups:

- Group A: €400,000 – Applies where the beneficiary is a child (including adopted or stepchild) of the disponer.

- Group B: €40,000 – Applies to siblings, nieces, nephews, grandchildren, and other relatives.

- Group C: €20,000 – Applies to all other relationships (non-relatives, friends, etc.).

Each person can receive gifts or inheritances up to their threshold from a group over their lifetime before paying CAT. Once the total value received exceeds the threshold, tax is payable at 33% on the excess.

Practical Example

Let’s say a parent leaves their child €500,000 in an inheritance:

- Group A threshold is €400,000.

- The taxable amount is €100,000.

- CAT due = €100,000 x 33% = €33,000.

What Assets Are Subject to CAT?

CAT applies to both movable and immovable assets:

- Immovable assets (e.g., property in Ireland) are always subject to CAT if located in Ireland.

- Movable assets (e.g., cash, shares) are taxable if either the disponer or the beneficiary is tax-resident or ordinarily resident in Ireland.

Common Exemptions and Reliefs

There are several exemptions and reliefs available under Irish tax law:

1. Spousal Exemption

Gifts or inheritances between spouses or civil partners are fully exempt from CAT.

2. Dwelling House Exemption

If certain conditions are met, a beneficiary may inherit a property without paying CAT. Conditions include:

- The property was the disponer’s main residence.

- The beneficiary lived in the house for at least 3 years before the disponer’s death.

- The beneficiary does not own or inherit another property.

- The property is retained for 6 years after inheritance.

3. Business Relief

Provides a 90% reduction in the taxable value of a business or farm transferred as a gift or inheritance. Conditions must be met around ownership, active use, and retention.

4. Agricultural Relief

Also offers a 90% reduction on qualifying agricultural property, subject to farming activity tests and retention rules.

5. Small Gift Exemption

Each person can receive up to €3,000 annually from any one donor without it affecting their group threshold or incurring CAT.

Planning Ahead

Effective estate and tax planning can significantly reduce CAT exposure. Some key strategies include:

- Lifetime gifting: Spreading out gifts over time to take advantage of thresholds and small gift exemptions.

- Utilising reliefs: Structuring business or farm succession to qualify for reliefs.

- Establishing trusts: In certain cases, trusts can provide control over assets while planning for tax-efficient succession.

CAT Deadlines and Filing

Beneficiaries are responsible for calculating and paying CAT. Key deadlines:

- Pay and file deadline: October 31 of the year following the valuation date (usually the date the gift or inheritance is received).

- Returns are filed through Revenue's ROS (Revenue Online Service).

Late payment may result in interest and penalties.

Final Thoughts

Capital Acquisitions Tax plays a significant role in wealth transfer planning in Ireland. With rates remaining steady and thresholds relatively low compared to property values, many beneficiaries find themselves liable for CAT even on modest inheritances.

Being proactive, seeking professional advice, and understanding the reliefs available are essential steps for any individual or family wishing to pass on wealth effectively and responsibly. Whether you're a beneficiary, a business owner planning for succession, or a parent thinking ahead, understanding CAT is key to preserving the legacy you've built.

If you have any concerns and require support with inheritance tax planning, get in touch, we’re here to help.

Recent posts.

Explore related articles for essential news and insights.

.png)

.png)